Written by Sandra Wolf - Mallowstreet

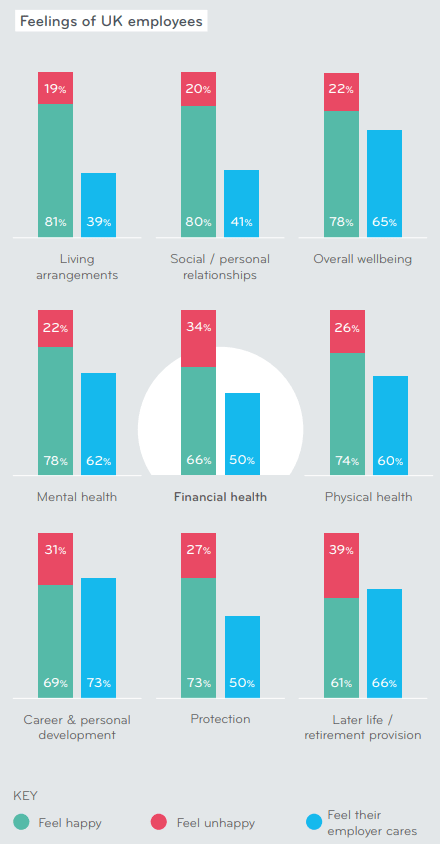

Financial wellbeing is considered a key factor to improving employee productivity, but trustees have traditionally kept at arm’s length from employer interventions. Should this be changing and what might work? Money worries keep many people up at night and cause them stress during the day. For nearly a quarter of UK adults an unexpected bill of £300, for example, would mean having to borrow or being unable to pay, according to the FCA.

In 1996, researchers from Virginia Tech found that the cost of to employers from employees’ poor financial behaviours was substantial, and their impact ranged from absenteeism and low morale to substance abuse, theft from employers or even suicide, and the issue has started to come to the attention of employers over here.

Are trustees becoming more involved in financial wellbeing? While traditionally there has been very little involvement of trustees in employer strategies, there are early signs that this might be changing. “Trustees being involved is the exception rather than the rule,” says senior consultant at PS Aspire, Stuart Arnold, but adds: “With pensions becoming a much bigger part of employee benefits we see employers looking at this as a bigger part of their wellbeing strategy.” Where the trustees are asked to help, this might now happen at an earlier stage than it did in the past, and there are event some trustee-led initiatives, he says. The fact financial wellness is being considered more, and together with pensions, is partly down to the influence of master trusts and group personal pension providers, which have more focused communication strategies when it comes to financial wellbeing, he says. Trustees can play a big role in engaging employees because they have access to every scheme member and people generally like to hear from them as well as the employer, but Arnold warns that communications need to be “little and often” so people are not overwhelmed. Technology will also play a key part, particularly by helping to aggregate information and bring pensions into the mainstream; Lloyds Bank provides an example by allowing customers with a Scottish Widows pension to see this on the same screen as their bank balance.

Giving access to advice: Damned if you do, damned if you don’t? Trustees have however to date not been very involved in such initiatives, agrees Heidi Allan, a senior financial wellbeing consultant at LCP, but “in more recent times we are starting to see them have a slightly greater awareness”. She believes there is an untapped opportunity for offering financial wellbeing messages to help people think less about pensions and more about their ability to save in the short, medium and long term. Even for deferred members a simple question on their annual benefit statement, such as, ‘When did you last review your pension arrangements?’ could prompt someone to take a closer look, she believes. More trustees and employers have recently also put in place a financial adviser for their scheme members, something that was recommended in the Caroline Rookes review commissioned by the Pensions Regulator after the British Steel transfers scandal. However, Allan is sceptical. Since the Retail Distribution Review took effect in 2012, she says, there are not enough advisers in the market, while the options at retirement have become much more complex to advise on. “To be honest it’s time consuming and there are not many organisations that provide that type of service," she says. The Financial Conduct Authority is currently reviewing the market impact of the RDR, as well as its Financial Advice Market Review. The findings are expected to be published in autumn 2020. One advice firm that only works with occupational pension schemes is Wealth at Work. Its director Jonathan Watts-Lay is a firm believer in trustee-appointed advisers, pointing out the negotiation advantage of a scheme buying in bulk compared with a member of the public, even where the member foots the bill. While trustees used to generally be of the view that giving access to guidance and advice would expose them to risk, in the wake of British Steel this perception might be changing. “Now if they do nothing that equally exposes them to risk and arguably even more so,” says Watts-Lay. This is further highlighted by employee surveys, which show employees are crying out for advice on their finances. “Very few people offer guidance and advice, yet if you survey members it’s almost the top thing they’d like to have from a financial wellbeing perspective,” says Brian Henderson, director of consulting at Mercer.

Debt comes before pensions Out of all their wellbeing interventions, pensions are the biggest expense for employers already, but Henderson thinks employers could “shave some money off the pension cost” by for example choosing a multi-employer fund rather than running their own scheme, and put the money saved into something people value more. However, saving with 20% tax relief might not be appropriate when an employee owes debt at 25%, he notes, and so debt repayment needs to be a priority. “There is a hierarchy of things you should be doing and if you have debt, that is the first you should be doing,” says Henderson. Pilot schemes such as the sidecar programme by master trust Nest – which deducts small amounts from people’s wage and puts it into a liquid savings account – could be a solution but only if they recognise this. Debt is one of the things that will cause people to suffer financial stress, but although “most employers... have their physical and emotional health benefits lined up” this does not hold true for the financial side, he says. This can be a conscious decision; some employers are nervous about going down this route as it involves gathering personal financial data on employees, but Henderson says this is based on a poor understanding of how these services work. He envisages a future where companies might have oversight committees for employee wellbeing, similar to the pensions oversight committees that some employers set up after moving their scheme to a multi-employer arrangement. Technology will also play an increasingly important role, he adds. “In the next few years you will see some really clever things coming to market... the issue for trustees will be how do you keep pace with this, because the large master trusts are spending money on this.”

Can trustees be involved in financial wellbeing strategies and how? Jonathan Watts-LaySteve ButlerStephen BudgeCharles GoodmanPaul BudgenStefan Lundbergh

Leave A Comment